For high-income individuals, 2026 marks a shift in how tax-planning decisions should be made. While the rules governing Roth IRA conversions have not changed, the broader tax environment has.

>> See How OBBBA Changes Charitable Deductions

As a result, Roth conversions are no longer a simple “convert when possible” strategy. They require careful coordination with your income, deductions, and now more than ever, your investment activity. This article outlines how to approach Roth conversions in 2026, including how capital gains harvesting fits into the strategy.

Please note: These are complex decisions that differ for every investor. We strongly recommend that you consult your tax advisor before taking any actions.

Understanding the Basics of Roth IRA Conversions/What Hasn’t Changed

A Roth IRA conversion allows you to move funds from a traditional IRA into a Roth IRA. When you do this:

- The amount converted is taxed as ordinary income

- No income limits prevent you from converting

- You can convert at any age

- There is no early withdrawal penalty on the conversion itself

The Internal Revenue Service guides these rules, and they remain in place for 2026. Roth conversions remain widely available. The key decision is how to integrate them into your overall tax plan, and here’s why.

What Changed for 2026 & Why Coordination Matters More

Recent tax law changes under OBBBA affect tax brackets and effective rates, deduction structures and AGI-based limits, as well as charitable deduction dynamics. This matters because both Roth conversions and capital gains increase your taxable income.

In 2026, higher income can push you into higher tax brackets, reduce deductions, and trigger phaseouts. In other words, your focus must shift from isolated decisions to coordinated income management.

The Hidden Factor: Income Stacking

Did you know that the tax system layers income in a specific order? First comes ordinary income (including Roth conversions); on top of that, you have capital gains. What this means for you is that:

- A large Roth conversion can push your capital gains into higher tax rates

- Realizing gains can reduce how much Roth conversion you can do efficiently

This interaction is called income stacking, and it is central to 2026 planning.

The Right Way to Execute Roth Conversions in 2026

Here, then, is the best way to convert your Roth IRA in 2026.

1. Start with your tax bracket

The most effective strategy is to identify your current marginal tax bracket and to convert only enough to fill that bracket.

Avoid crossing into higher brackets unless there is a clear long-term benefit.

2. Time your decisions carefully

The best time to finalize decisions is typically late in the year (Q3–Q4) when your income picture is clear. This allows you to:

- Adjust for business income

- Account for capital gains

- Optimize deductions

3. Coordinate Roth conversions with capital gains

This is where most mistakes occur.

(Reminder: these are complex decisions that differ for every investor. We recommend that you consult your tax advisor before taking any actions.)

Default Strategy: Prioritize Roth Conversion

The default strategy (for most high-income clients) is to prioritize the Roth conversion, and then evaluate whether capital gains harvesting fits within remaining tax capacity. This works because:

- Roth conversions create permanent tax-free growth

- Capital gains can often be deferred

When to Harvest Capital Gains

You may want to harvest gains when you are in a lower-than-normal income year, your Roth conversion is limited or moderate, and you can stay within favorable capital gains rates.

Balanced Approach: Partial Roth Conversion AND Partial Gains Harvesting

In some cases, you can do both: a partial Roth conversion and a partial gains harvesting. This requires careful modeling to avoid crossing thresholds.

When to Hold Off

You will want to avoid harvesting gains in the following three situations:

- You are already in a high-income year

- You are executing a large Roth conversion

- Gains would push you into higher tax brackets or reduce deductions

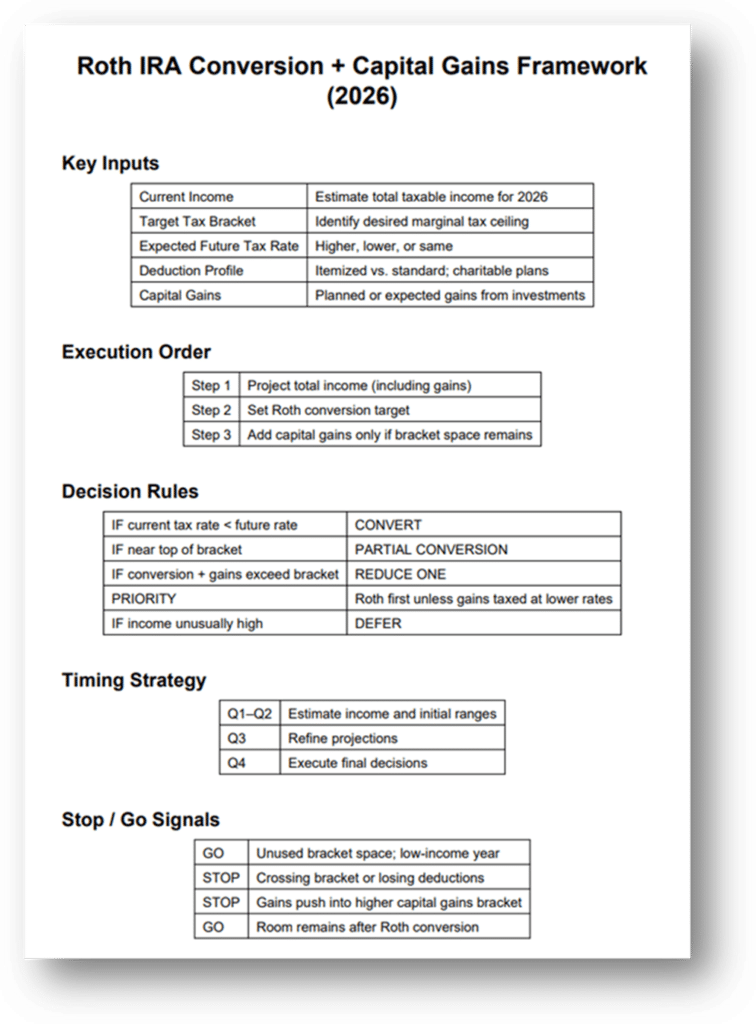

A Simple Decision Framework for Roth IRA Conversions

To help with this matter, here is a simple three-step decision framework.

Step 1: Estimate your total income

For this calculation, include your salary or business income, your planned Roth conversion, as well as any expected capital gains.

Step 2: Identify key thresholds

Here, you want to determine what key thresholds you fall into:

- Top of your current tax bracket

- Capital gains tax thresholds

- Deduction phaseouts

Step 3: Apply decision rules

In step 3, you apply the decision rules, which include whether to convert, defer, or something in between.

Consider converting if:

- You have room in your current bracket

- Your future tax rate is likely higher

Add capital gains if:

- You still have room after your Roth conversion

- Gains will not push you into higher tax rates

Pause or defer if:

Your combined income triggers higher brackets and/or loss of deductions.

Managing Your Plan Throughout the Year

You’ll definitely want to manage your plan throughout the year to help you apply the decision rules as this is where are best able to optimize.

Early in the year: estimate your income, and identify a preliminary Roth conversion range.

Mid-year: adjust for market activity and business performance.

Year-end: finalize your Roth conversion amount and what capital gains you will realize.

Common Mistakes to Avoid:

- Don’t treat Roth conversions and capital gains separately

- Don’t overload one year with both

- Be sure not to ignore how gains affect your Roth strategy

- Remember to revisit the plan throughout the year

Final Thoughts About Roth IRA Conversions in 2026

Roth IRA conversions remain one of the most effective long-term tax strategies. But in 2026, success depends on coordination. The goal is not to maximize any single move. Rather, it is to:

- Manage income deliberately

- Use tax brackets efficiently

- Align investment and tax decisions

When Roth conversions and capital gains harvesting are coordinated properly, they create a more flexible, tax-efficient financial future.

Thanks for reading, and don’t hesitate to reach out with questions. We offer a Free Investor Consultation.

Article assumptions

We’ve made the following assumptions in this article:

- Roth conversion rules remain unchanged under current IRS guidance

- Capital gains are primarily long-term

- Focus is on federal tax strategy

Art Credit: Peasant Woman in Conversation with a Boy, print, 18th century, Harvard Art Museum, Fogg Museum, https://hvrd.art/o/246754

Note: This blog article is intended for general informational purposes only. Nothing in it should be construed as, and may not be used in connection with, an offer to sell, or a solicitation of an offer to buy or hold, an interest in any security or investment product. Investing involves risk.

References:

OBBBA – PUBLIC LAW 119–21—JULY 4, 2025 (pdf)

Working Families Tax Cuts – Individuals and workers

Questions and Answers on the Net Investment Income Tax

Retirement plan and IRA required minimum distributions FAQs

Rollovers of after-tax contributions in retirement plans

IRA FAQs – Distributions (withdrawals)

About Form 8606, Nondeductible IRAs

Instructions for Form 6251 (2025) Alternative Minimum Tax—Individuals

2025 Instructions for Form 8960 Net Investment Income Tax—Individuals, Estates, and Trusts (pdf)

Contributions to Individual Retirement Arrangements (IRAs) – 2025 (pdf)

Publication 590-B Distributions from Individual Retirement Arrangements (IRAs) 2025 (pdf)

Medicare & Social Security Related: